Markets Pulse

AI Pulse June 9, 2026

EXECUTIVE SUMMARY

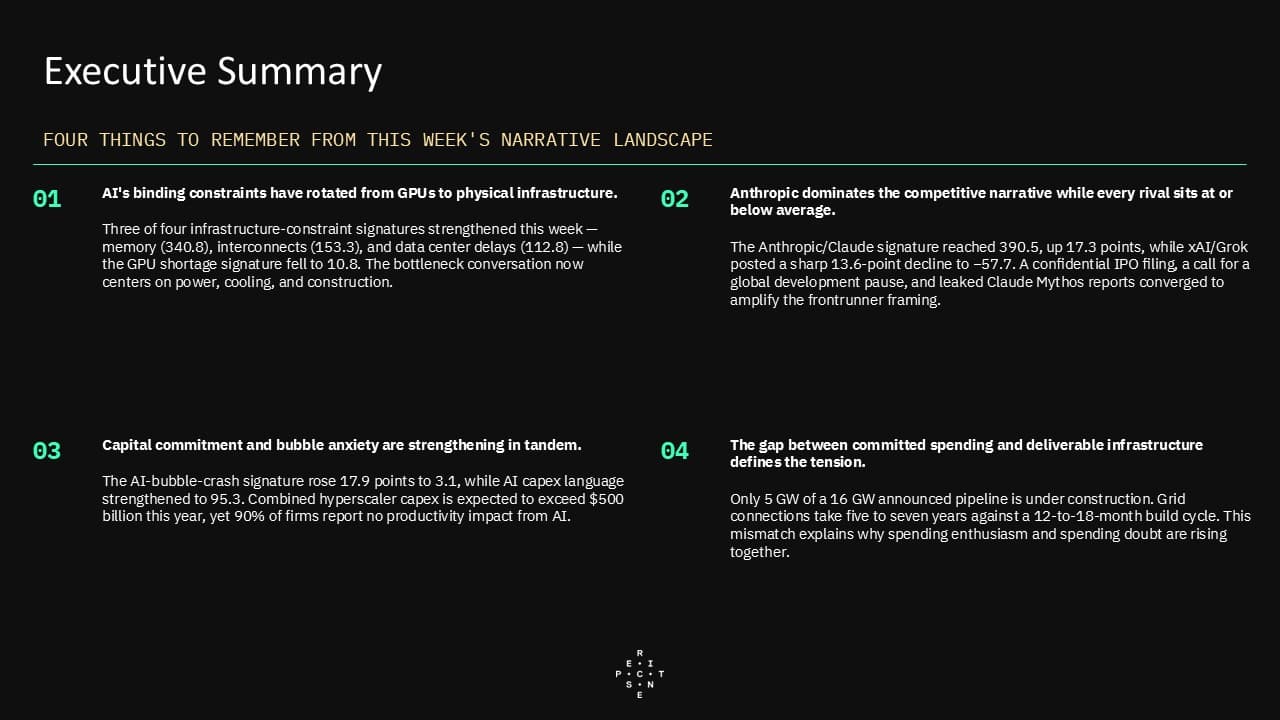

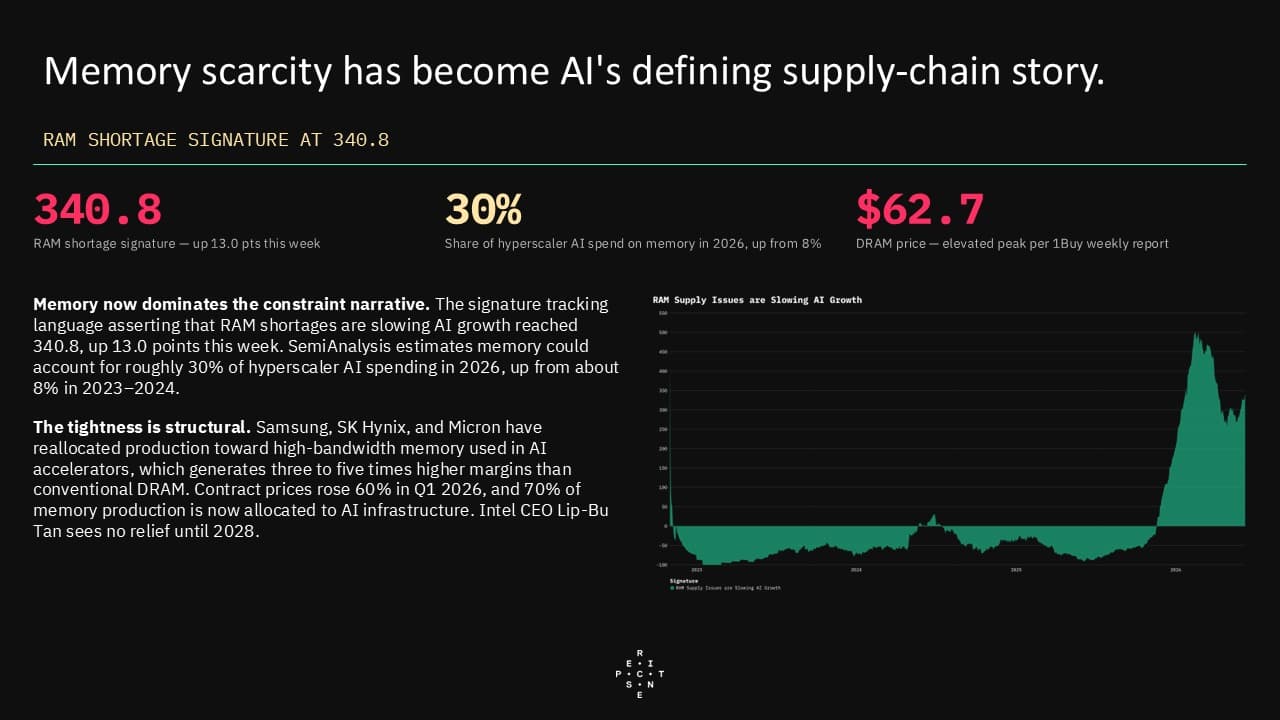

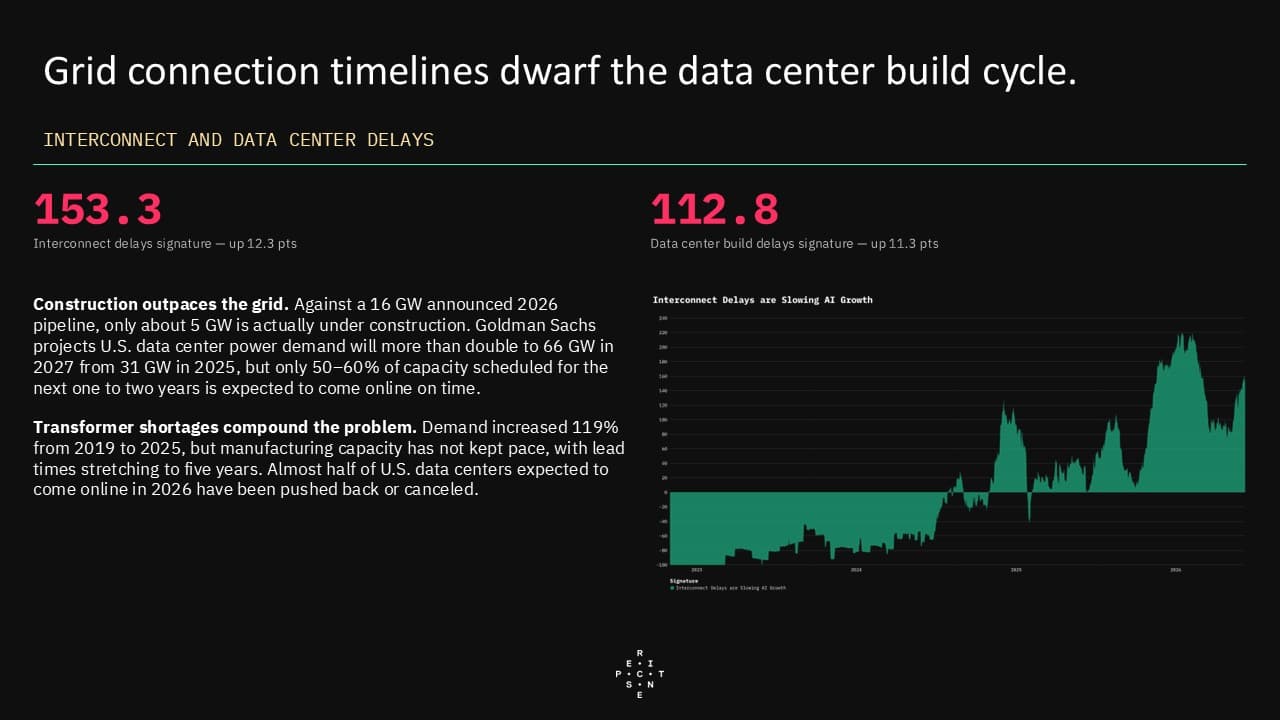

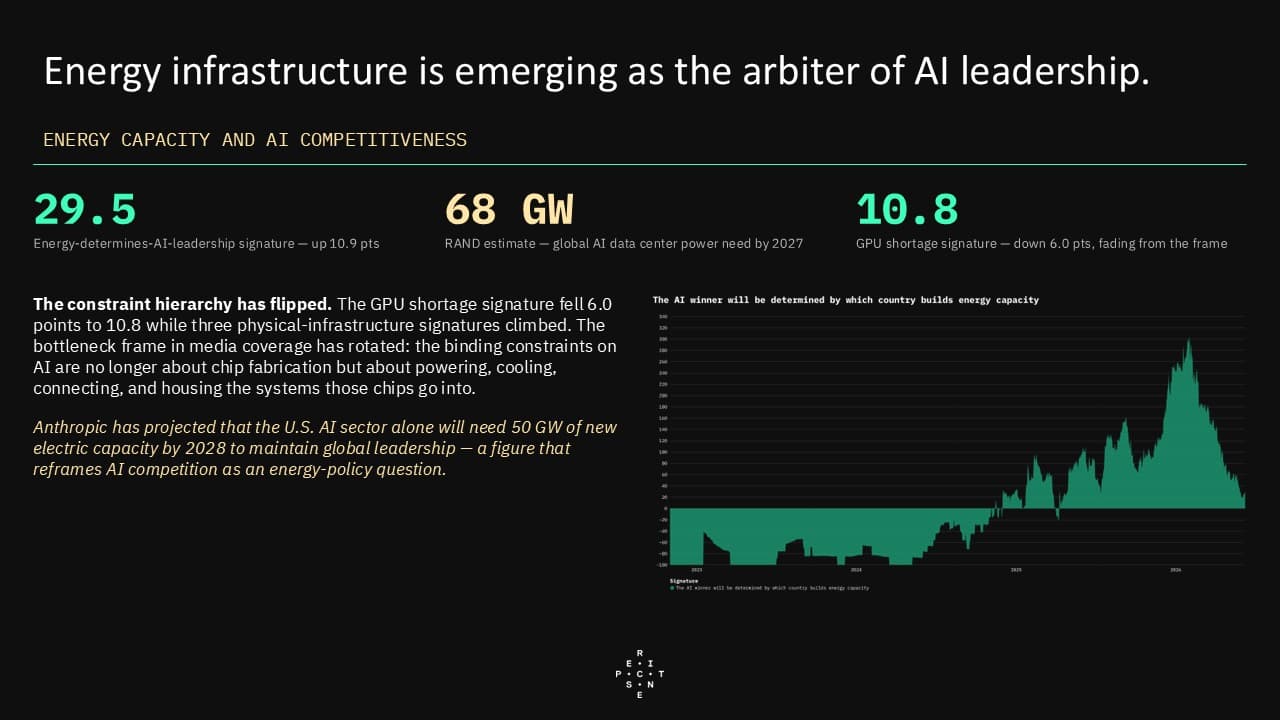

- The media framing of AI's binding constraints has rotated decisively away from GPU shortages and toward physical infrastructure — memory, power grid interconnects, and data center construction. Three of Perscient's four infrastructure-constraint semantic signatures strengthened this week, all at elevated absolute levels, while the GPU shortage signature declined. Memory now accounts for a far larger share of hyperscaler AI spending than it did even two years ago, DRAM prices have reached record highs, and industry leaders see no relief until 2028. Meanwhile, only a fraction of announced data center capacity is actually under construction, and grid connection timelines of five to seven years dwarf the 12-to-18-month construction cycle — a mismatch that is drawing increasing media attention to the proposition that energy infrastructure will determine AI leadership.

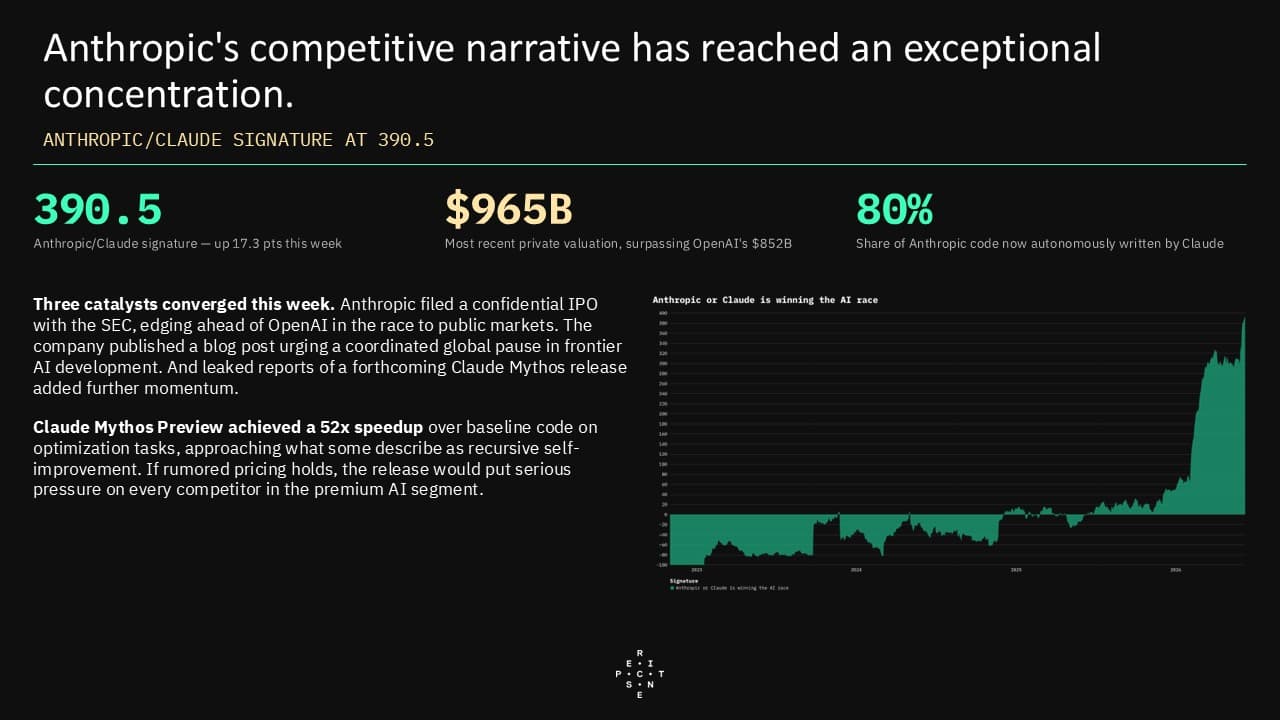

- Anthropic has consolidated a strikingly lopsided position in the competitive narrative, with its semantic signature at the highest absolute level in the full dataset and strengthening further this week. A confidential IPO filing, a public call for a global pause in frontier development, and leaked reports of a forthcoming Claude Mythos release converged to amplify the frontrunner framing. Every other competitor signature — OpenAI, xAI/Grok, and Deepseek/China — sits at or well below its long-term average, with the xAI/Grok signature posting the single largest weekly decline of any signature in the dataset. The degree of narrative concentration around a single company is unusual and raises the question of whether operational pressures and scaling frictions will eventually erode the goodwill that currently sustains it.

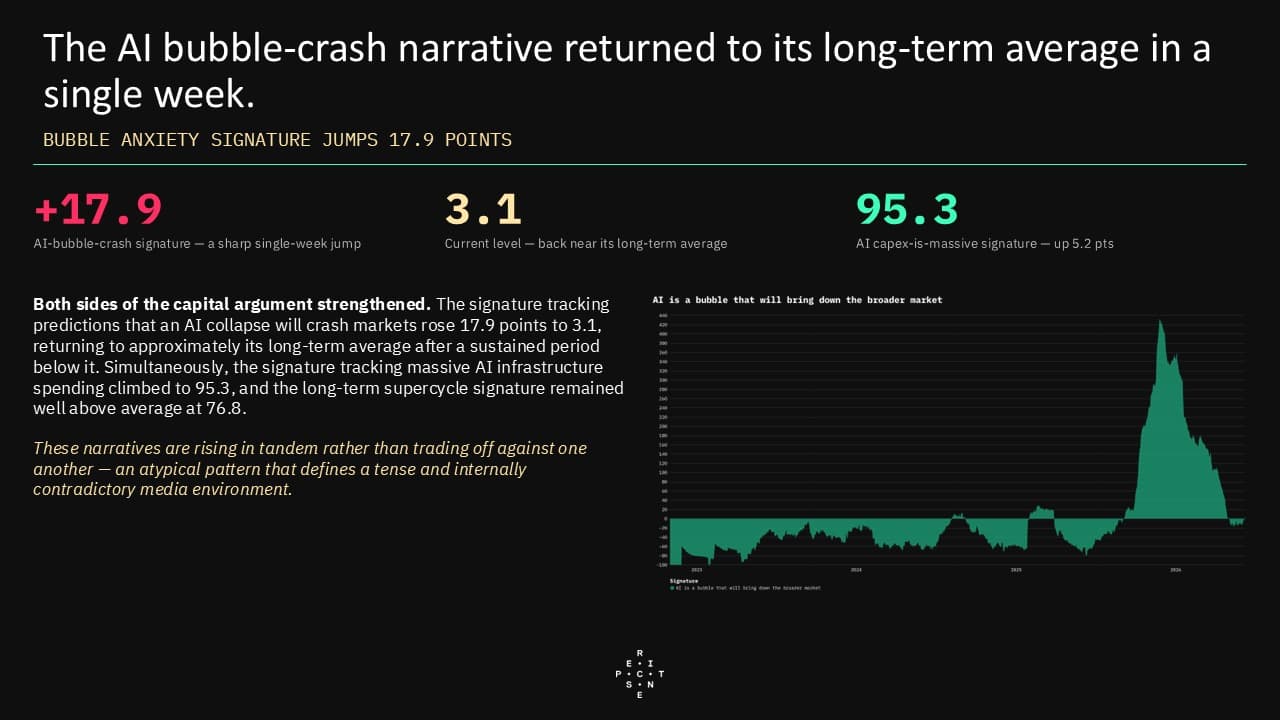

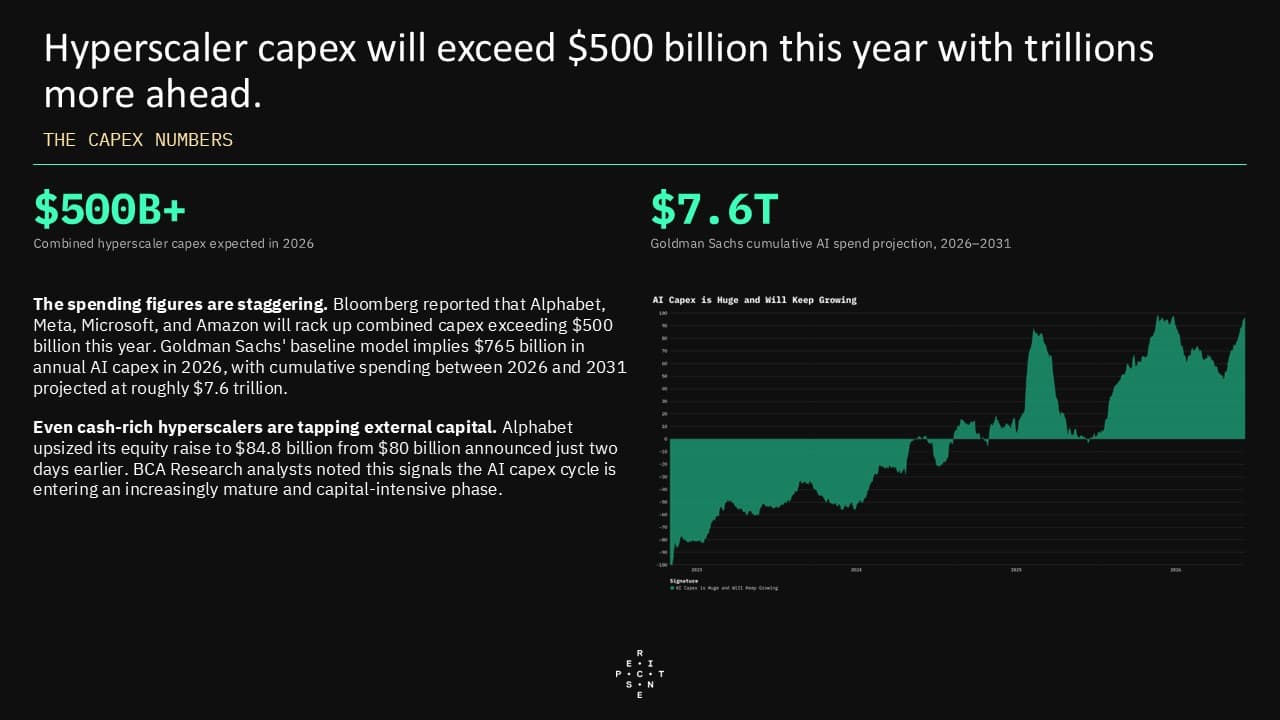

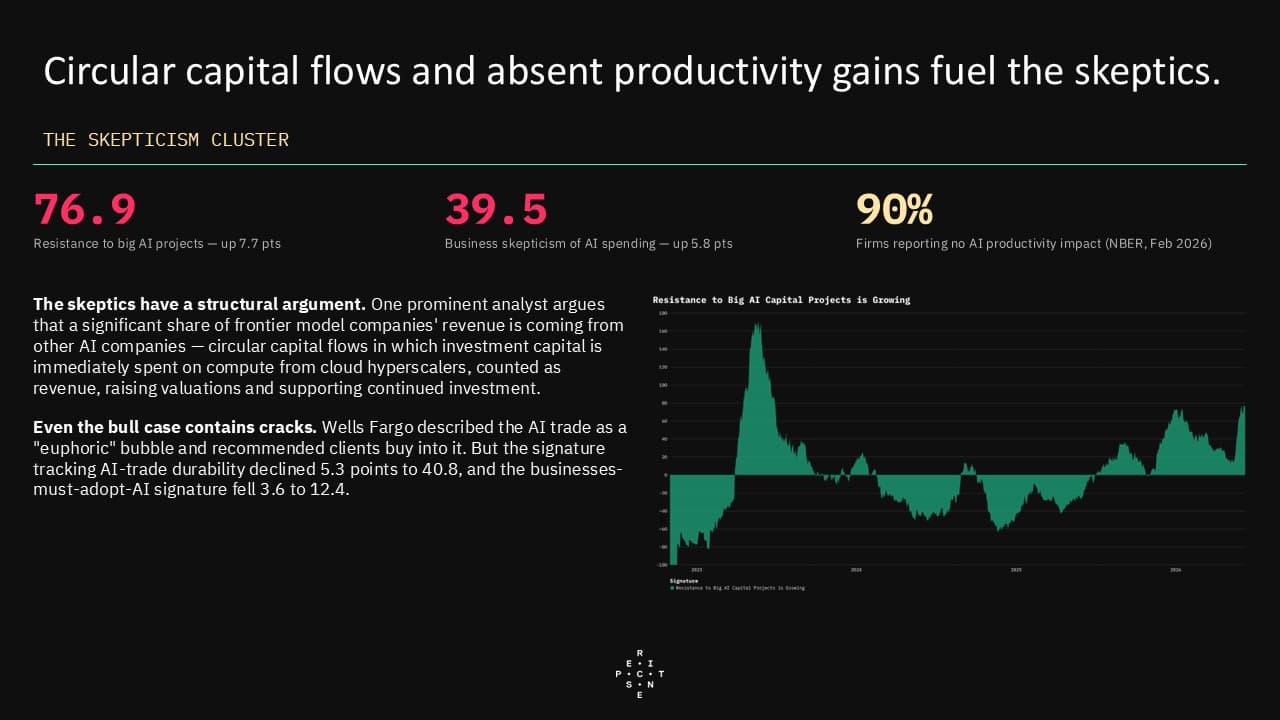

- Capital commitment and bubble anxiety are rising in tandem — an atypical pattern that defines a tense and internally contradictory media environment. Perscient's semantic signature tracking predictions that an AI investment collapse will crash overall markets recorded the single largest one-week increase of any signature, while signatures tracking massive infrastructure spending and the long-term investment supercycle also strengthened. Combined hyperscaler capex is expected to exceed $500 billion this year, and Goldman Sachs projects cumulative AI spending of roughly $7.6 trillion between 2026 and 2031. Yet critics point to circular capital flows among AI companies, an NBER study that found that 90% of firms report no productivity impact from AI, and growing doubt about whether announced investment will translate into realized returns.

- The physical bottleneck story and the capital story are deeply intertwined: the widening gap between committed spending and deliverable infrastructure is the thread that connects rising capex figures to rising skepticism. Hundreds of billions in announced investment confront grid delays, transformer shortages, and memory allocation constraints that prevent that capital from translating into operational capacity on schedule. This mismatch helps explain why the media can simultaneously describe AI investment as both immense and potentially fragile — and why signatures tracking spending enthusiasm and spending doubt both strengthened this week rather than trading off against one another.