Markets Pulse

AI Pulse June 16, 2026

EXECUTIVE SUMMARY

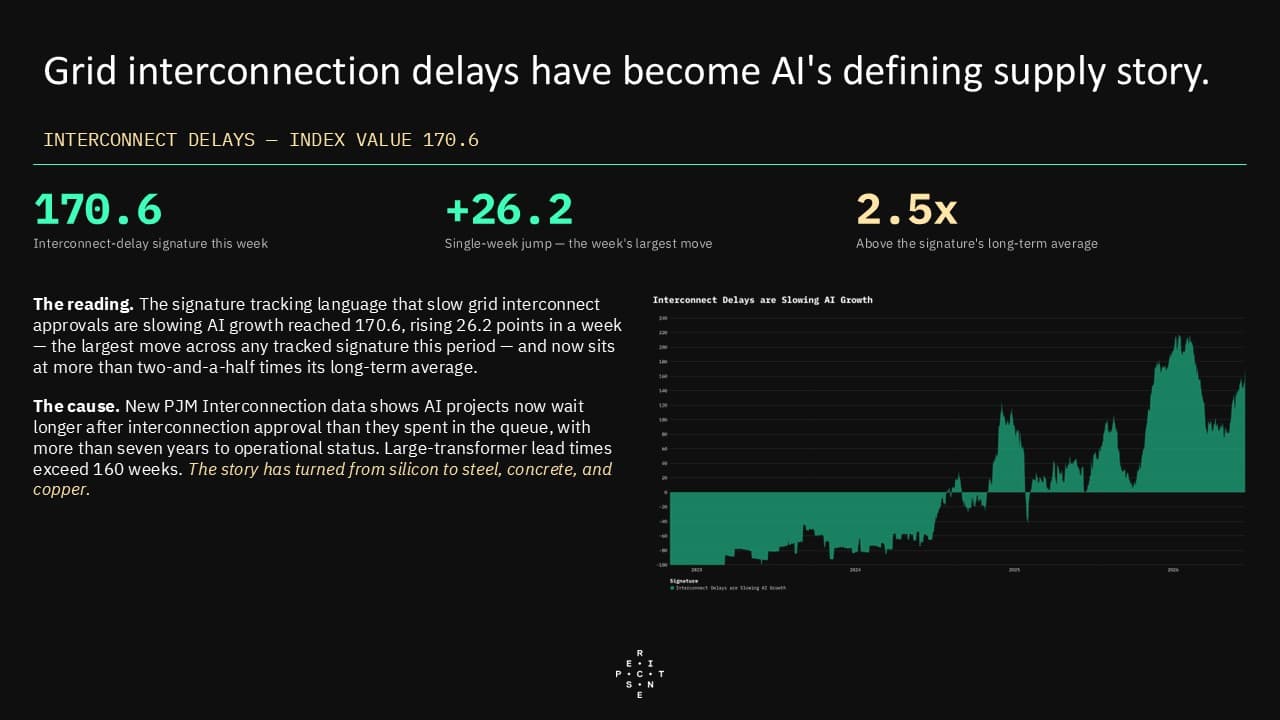

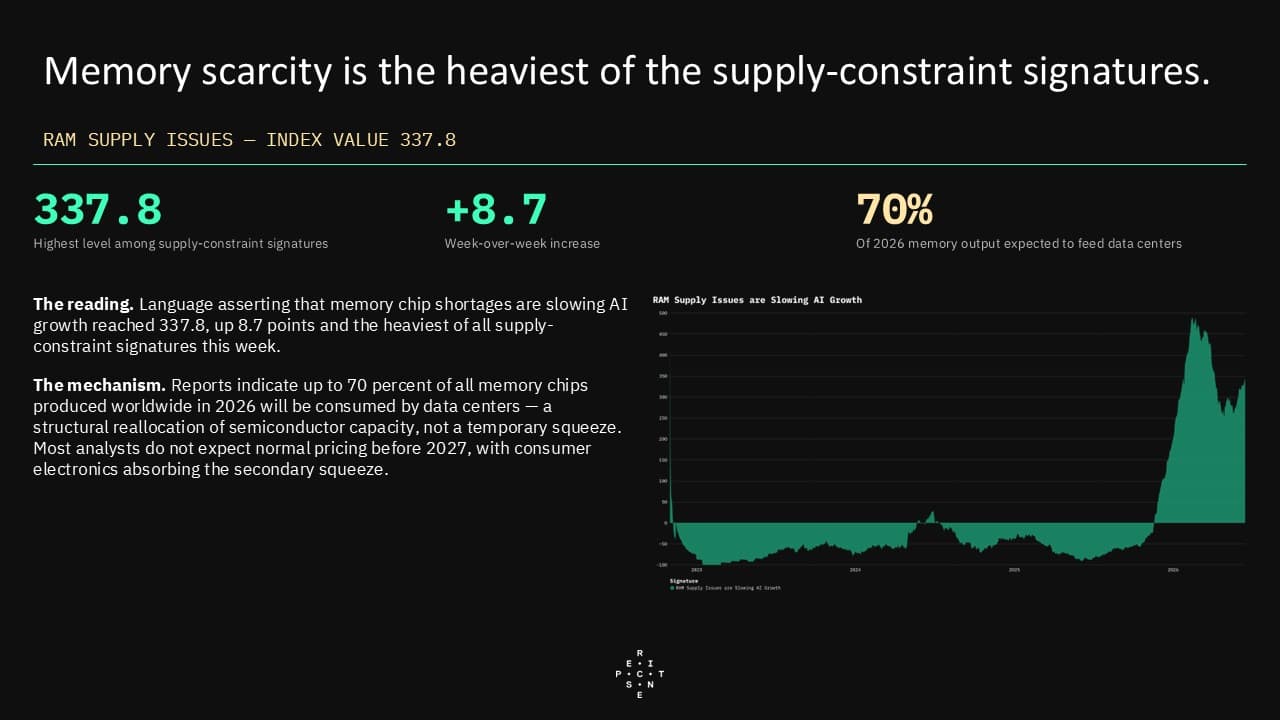

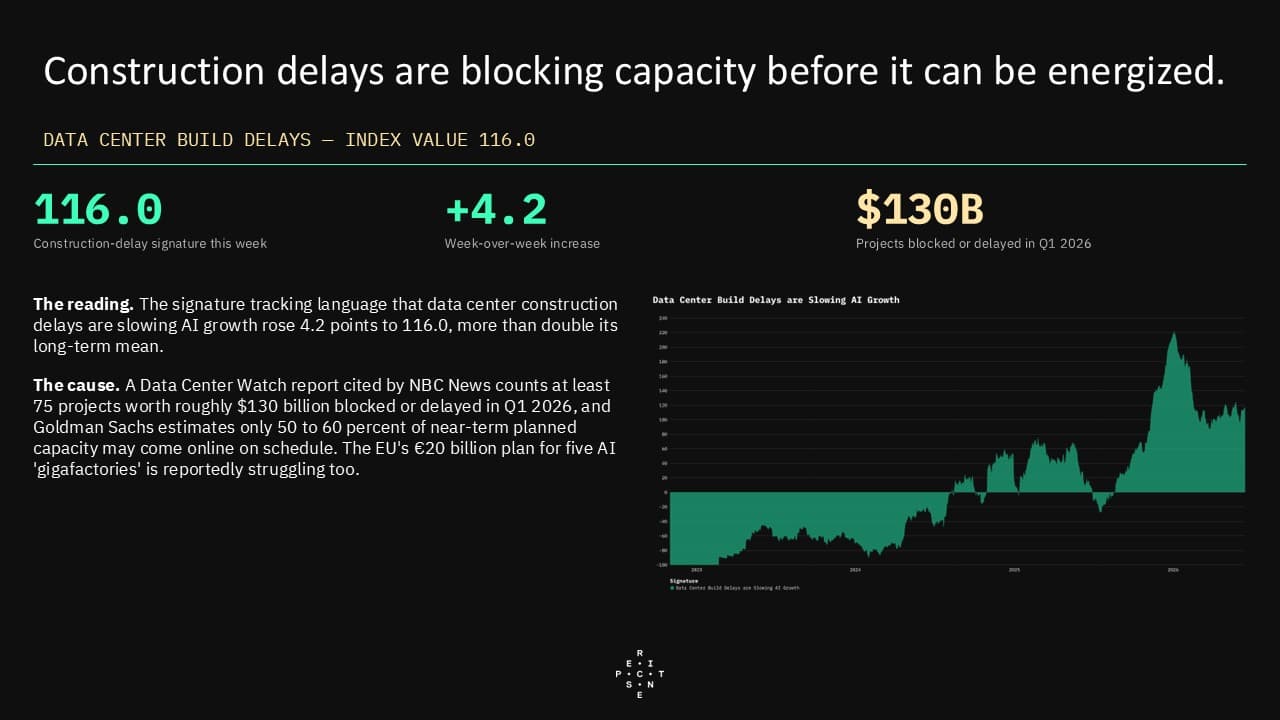

- The binding constraint on AI expansion has migrated from chip supply to physical infrastructure. Media language about grid interconnection delays surged to more than two-and-a-half times its long-term average, recording the largest single-week increase across all tracked signatures, while GPU shortage language fell back to baseline levels. Memory chip shortages, data center construction delays, power transformer lead times exceeding 160 weeks, and public opposition to data center siting now dominate coverage of the gap between announced AI ambitions and operational capacity—a shift that reframes the AI growth story from a semiconductor narrative to an energy, construction, and permitting narrative.

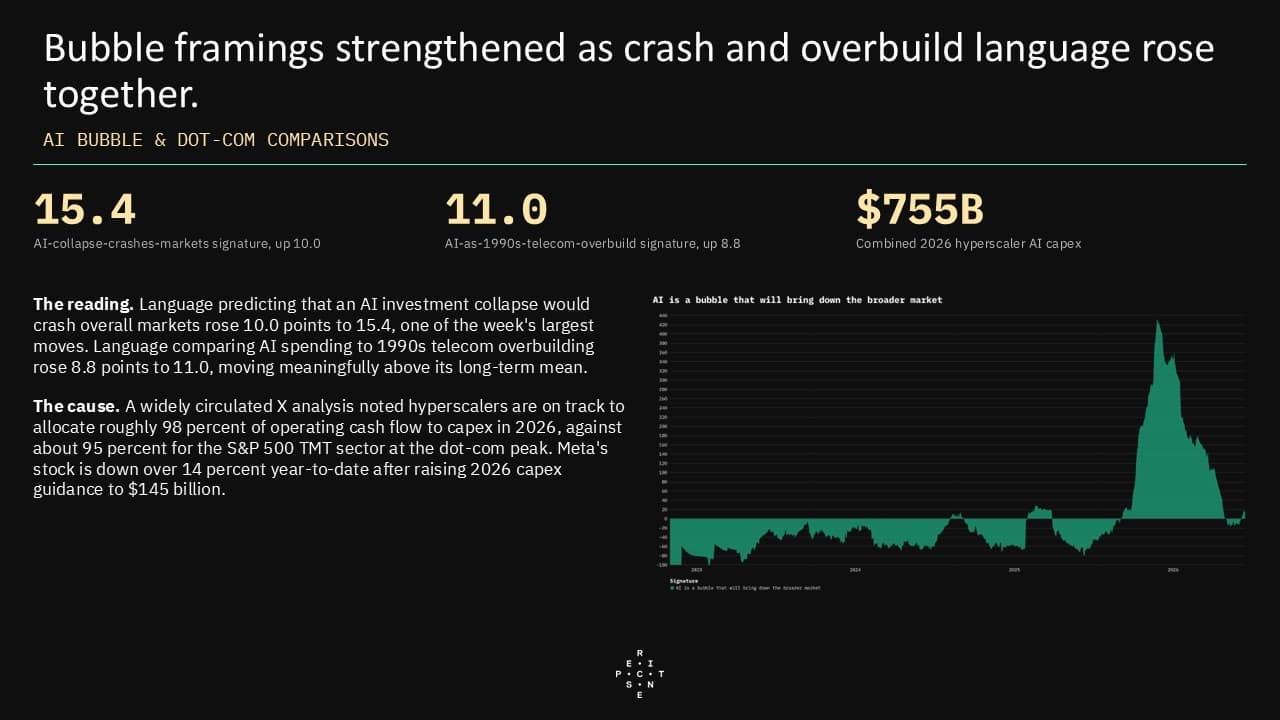

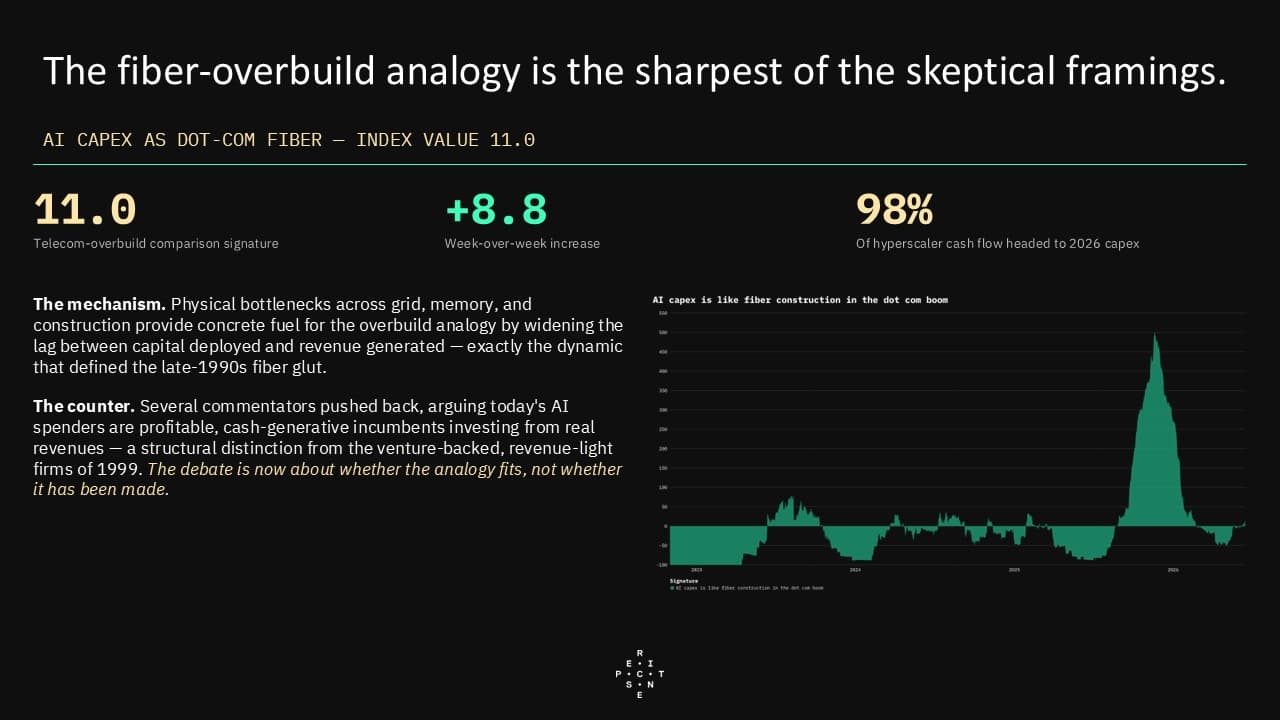

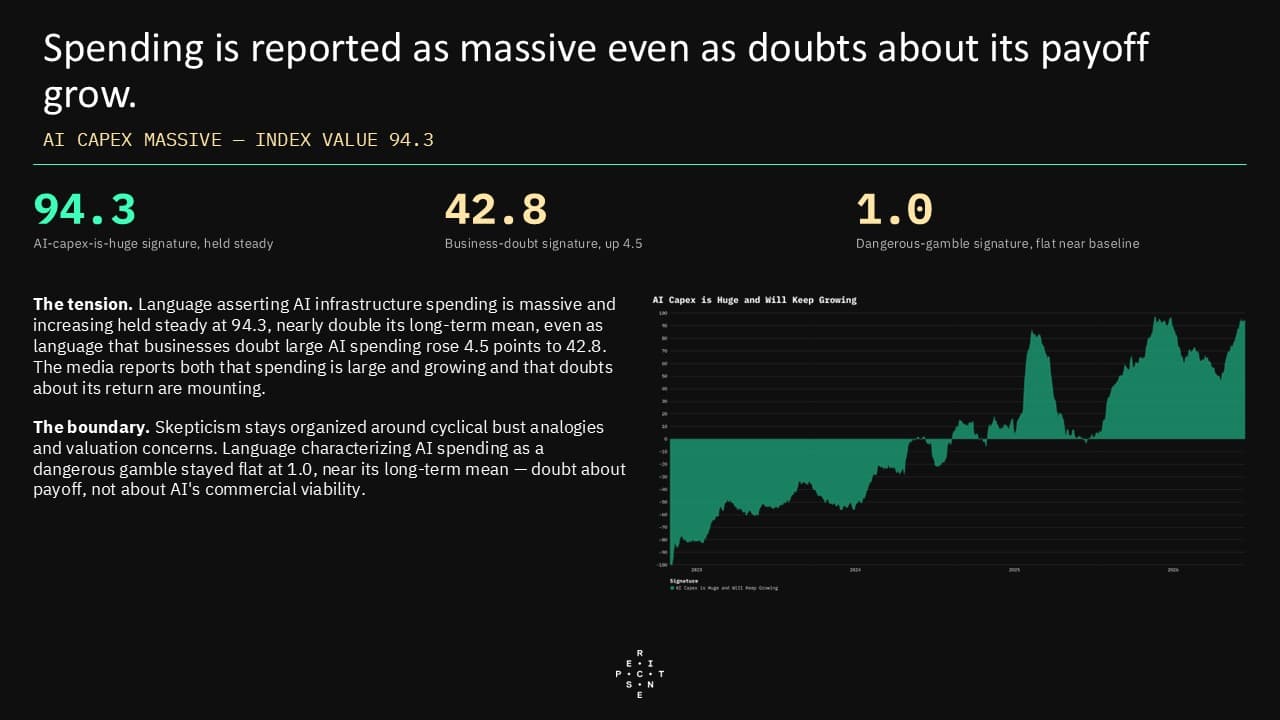

- Dot-com comparisons and bubble rhetoric are strengthening in tandem, even as media coverage continues to characterize AI spending as massive and growing. Language comparing current AI capital expenditure to 1990s telecom overbuilding and language predicting that an AI investment collapse could crash broader markets both rose materially, while bull-case signatures tracking "supercycle" and "durable investment theme" language softened. This creates a pronounced narrative tension: the same media environment that reports $755 billion in combined hyperscaler spending is increasingly questioning whether that spending will produce commensurate returns. The physical infrastructure bottlenecks documented across grid, memory, and construction signatures provide concrete fuel for these skeptical framings by widening the lag between capital deployed and revenue generated.

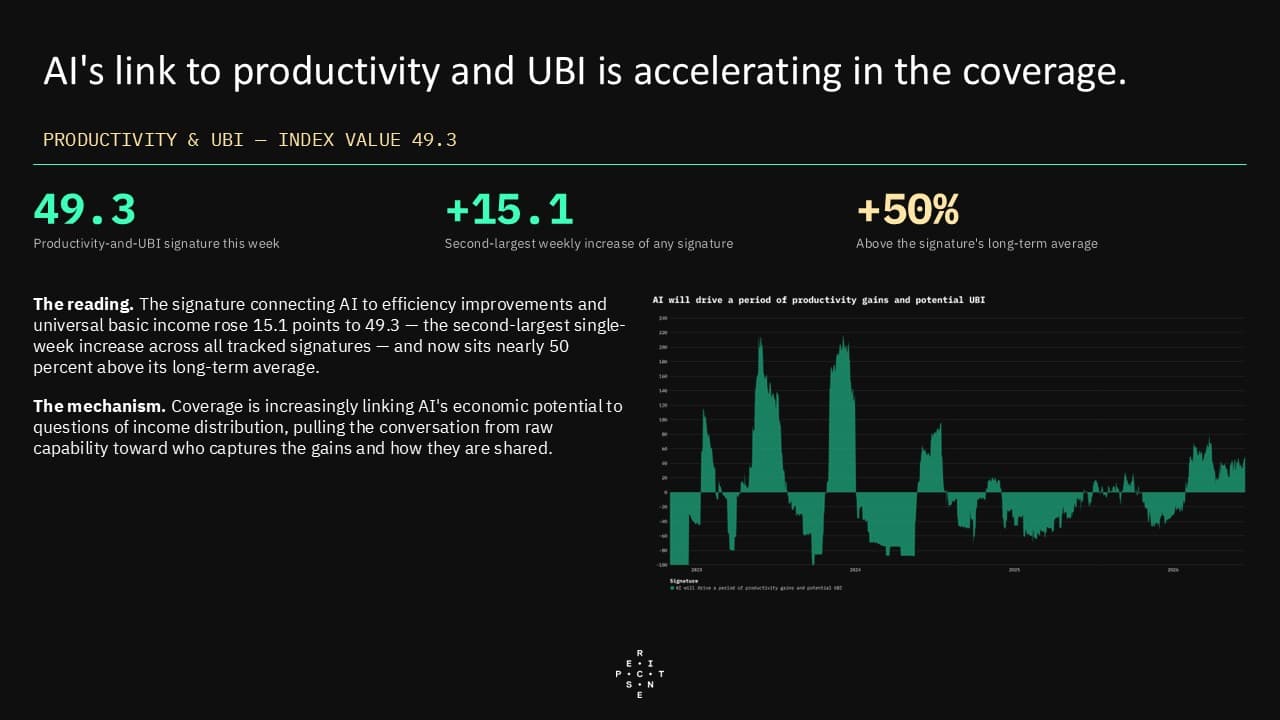

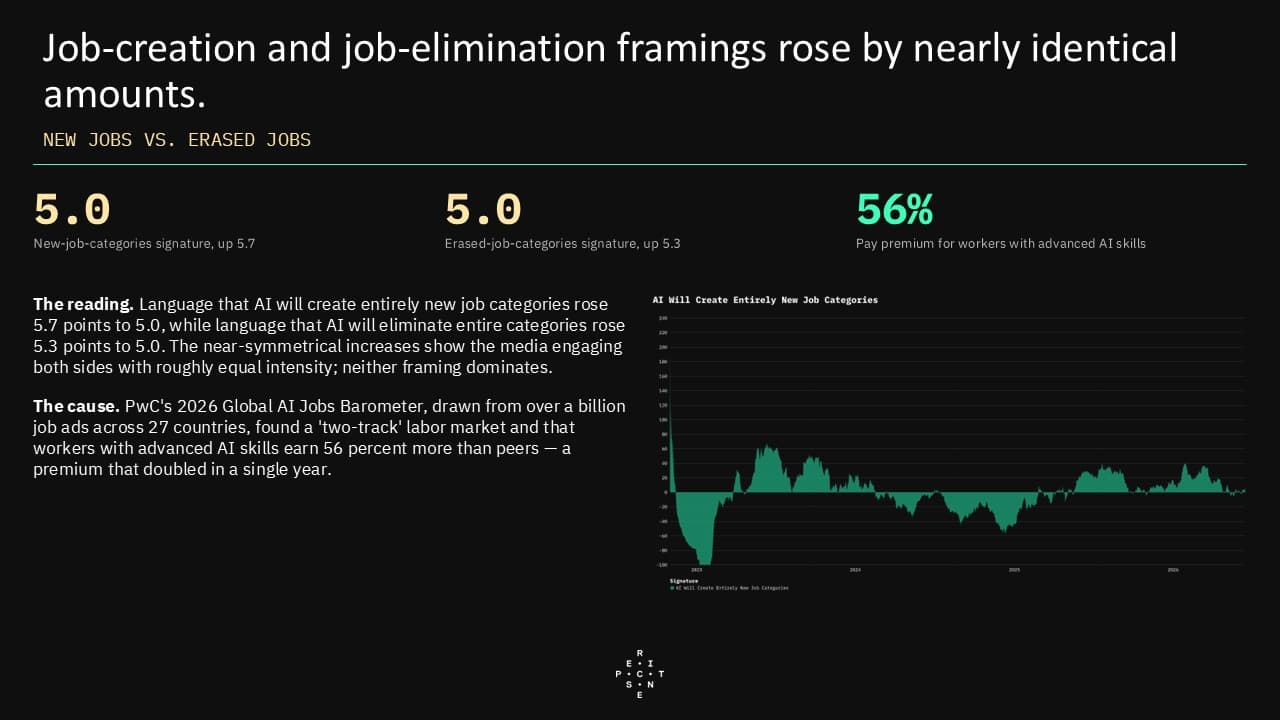

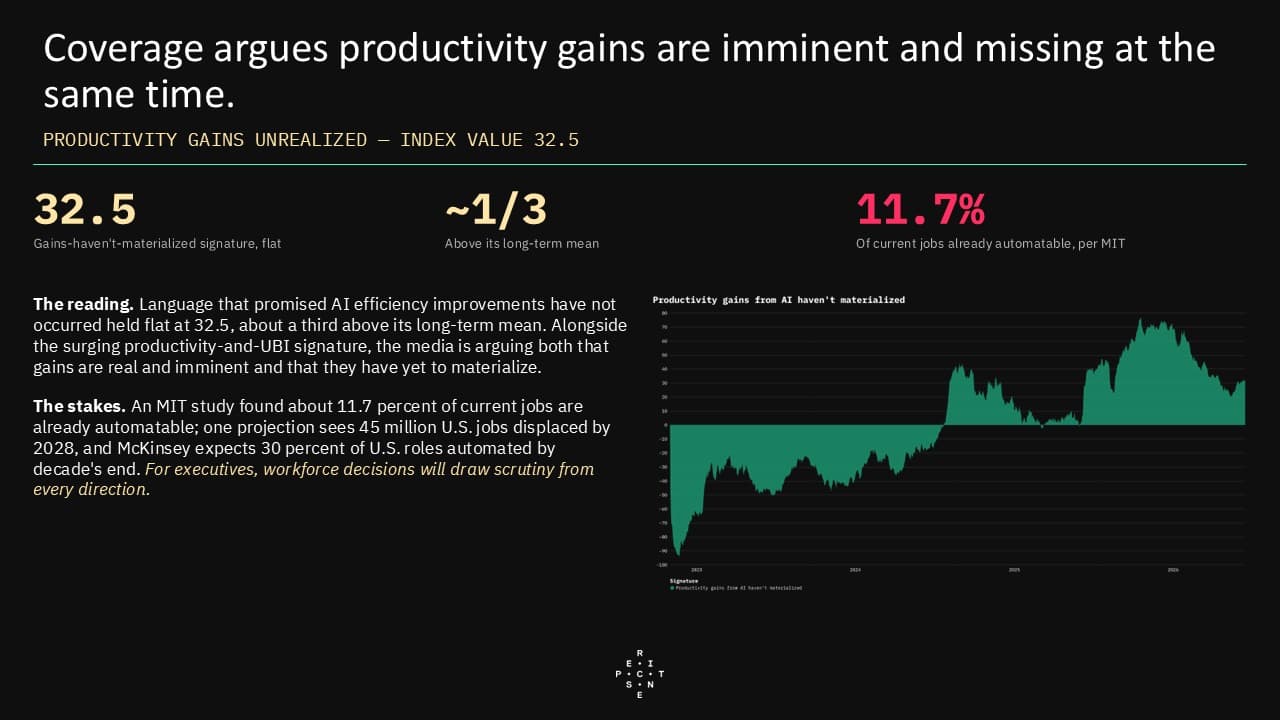

- The labor market debate around AI intensified sharply in both directions, with no dominant framing emerging. Language linking AI to efficiency gains and universal basic income recorded the second-largest weekly increase of any tracked signature, while language predicting that AI will create entirely new job categories and language predicting that AI will eliminate entire categories rose by nearly identical amounts. PwC data showing that workers with advanced AI skills earn a 56 percent premium coexists with projections that tens of millions of jobs face displacement—an unresolved tension that leaves corporate workforce decisions exposed to scrutiny regardless of direction.

- Across all three major narrative domains—infrastructure, investment sustainability, and labor—media coverage is escalating intensity without converging on consensus. Skepticism remains organized around cyclical bust analogies and valuation concerns rather than outright rejection of AI's commercial viability; language characterizing AI infrastructure spending as a dangerous gamble stayed near baseline. The simultaneous elevation of constraint, doubt, and opportunity signatures suggests that the media environment is pricing in execution risk and distributional uncertainty far more than it is questioning whether AI itself will prove consequential.