Private Credit Pulse May 19, 2026

June 2, 2026

Executive Summary

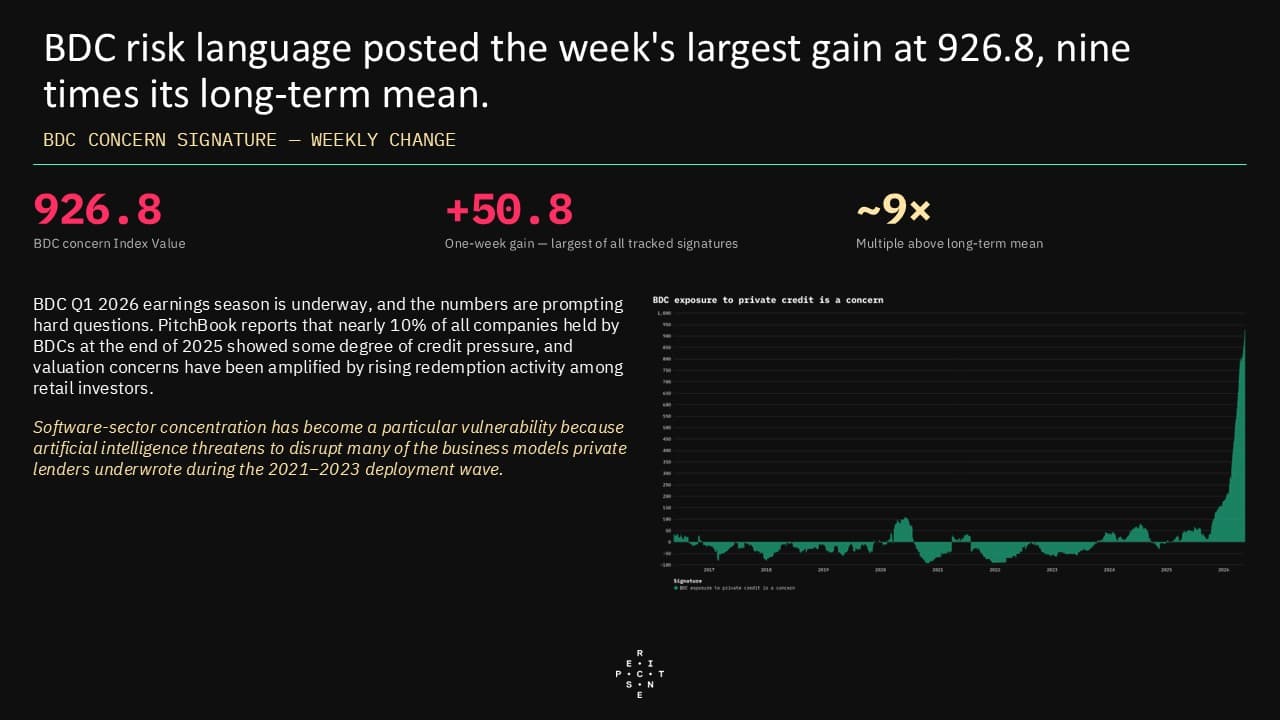

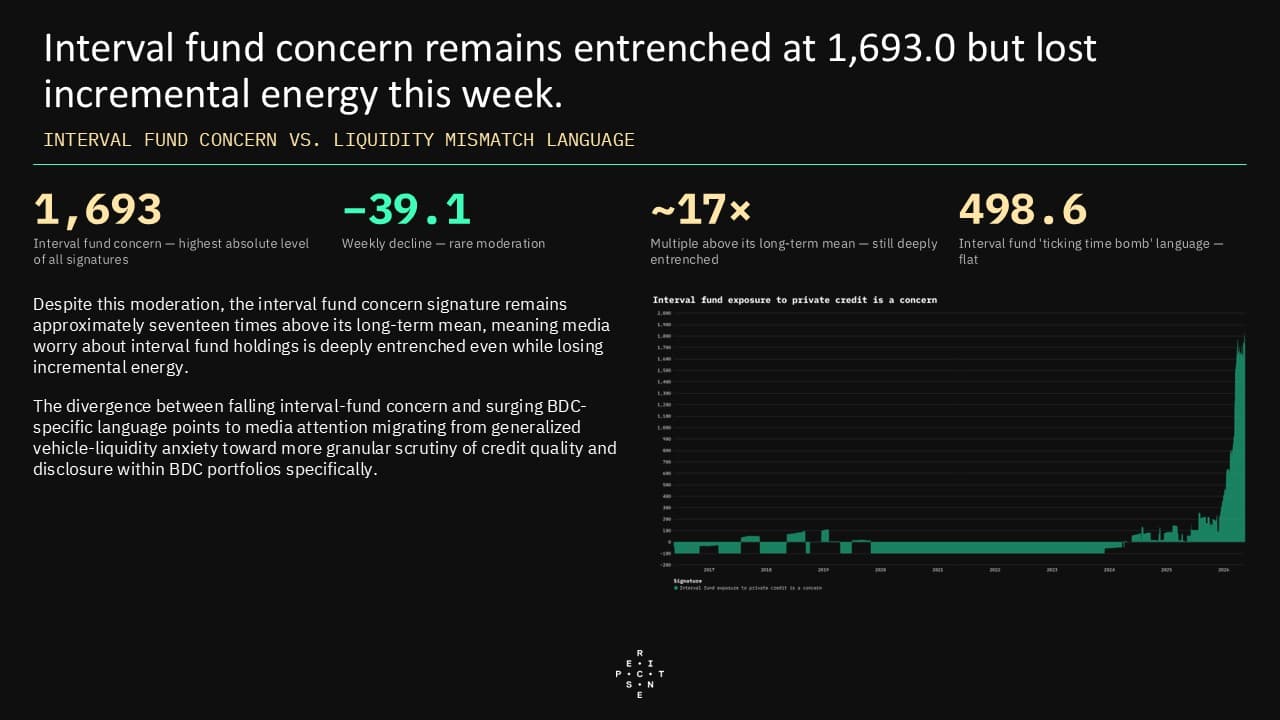

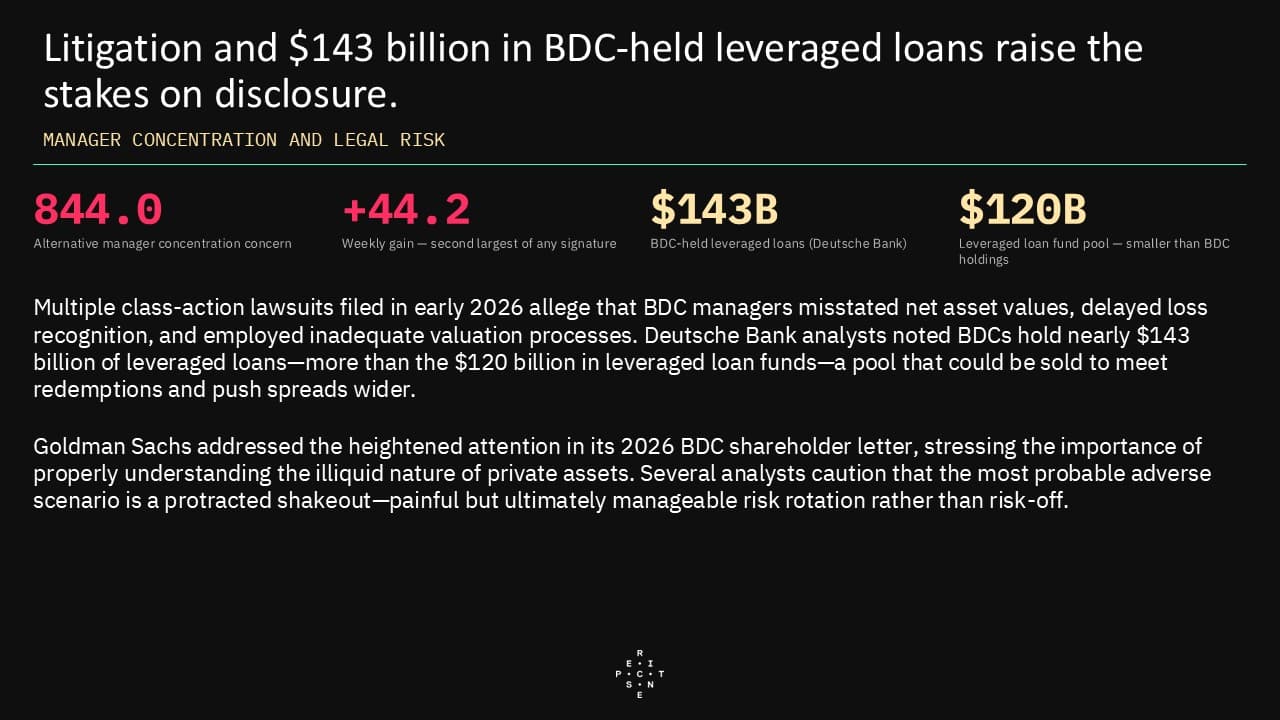

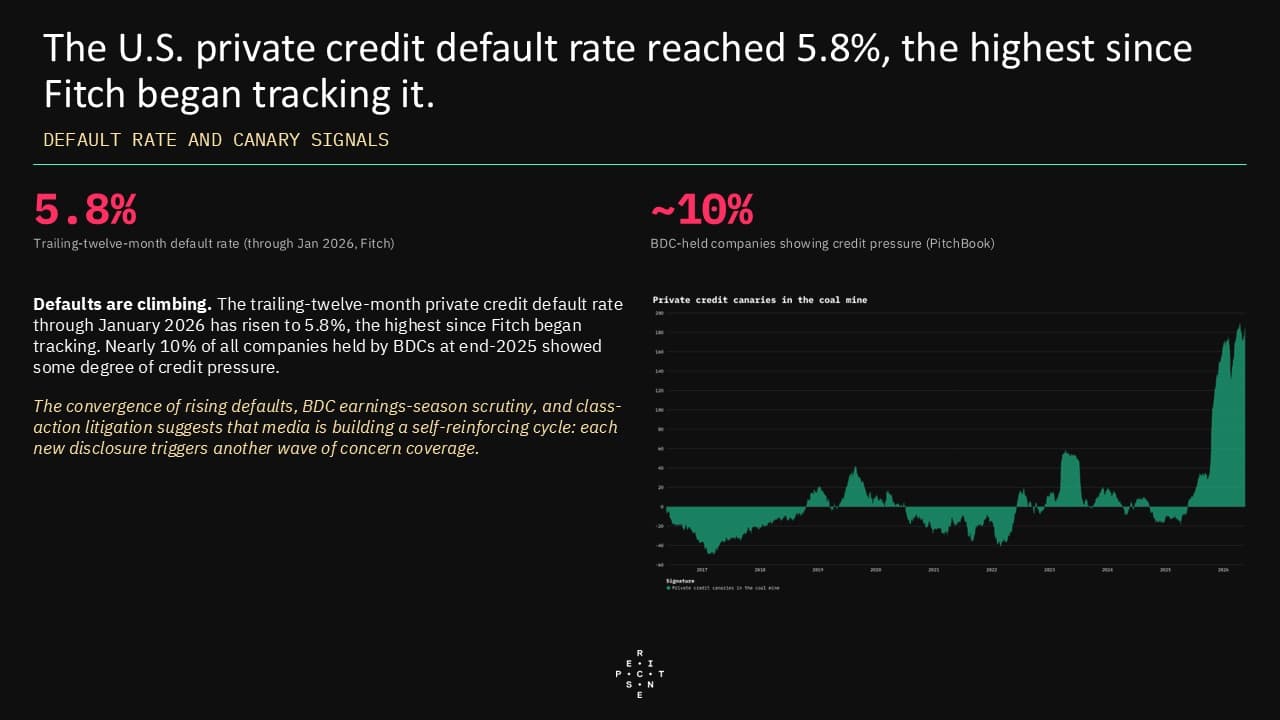

- Media concern has rotated from generalized interval-fund liquidity anxiety toward granular scrutiny of BDC credit quality, disclosure practices, and manager concentration. BDC earnings season, a trailing-twelve-month default rate at its highest level since tracking began, and class-action litigation alleging misstated net asset values are fueling this shift. The interval-fund concern narrative—though still deeply entrenched at extreme levels—lost incremental energy, while Perscient's semantic signatures for BDC risk and alternative-manager concentration posted the two largest weekly gains of any tracked signatures.

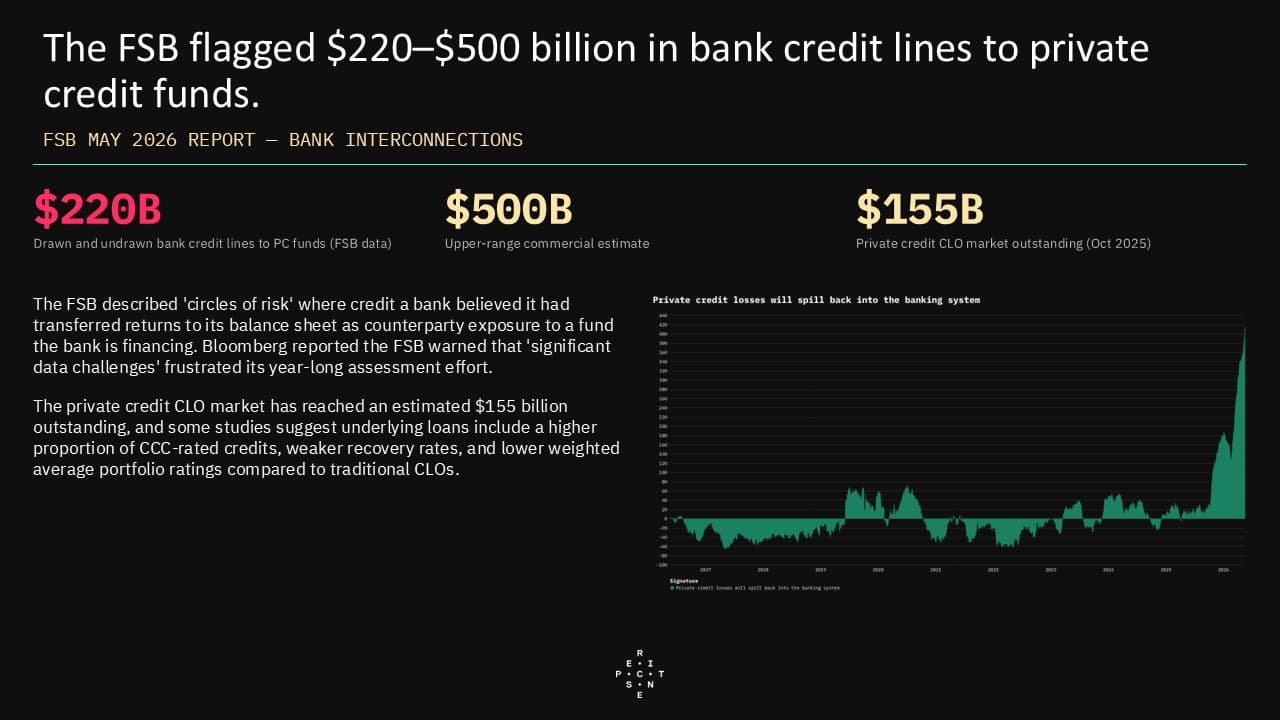

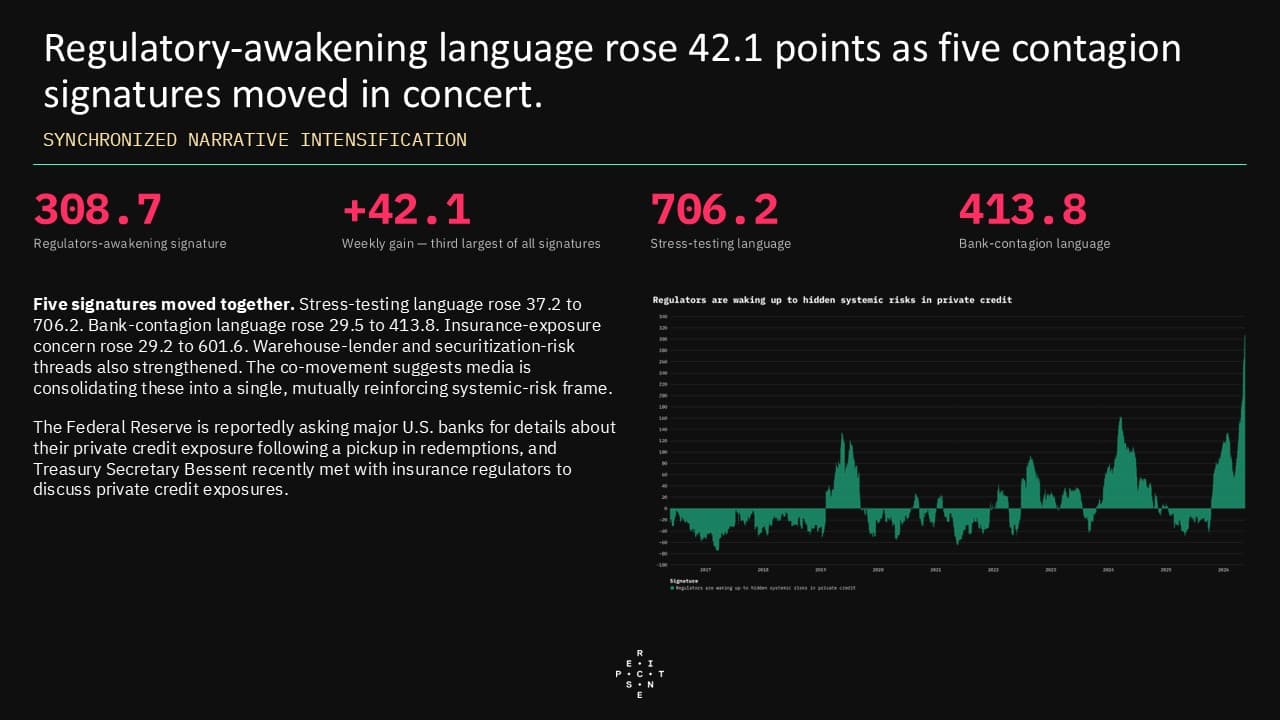

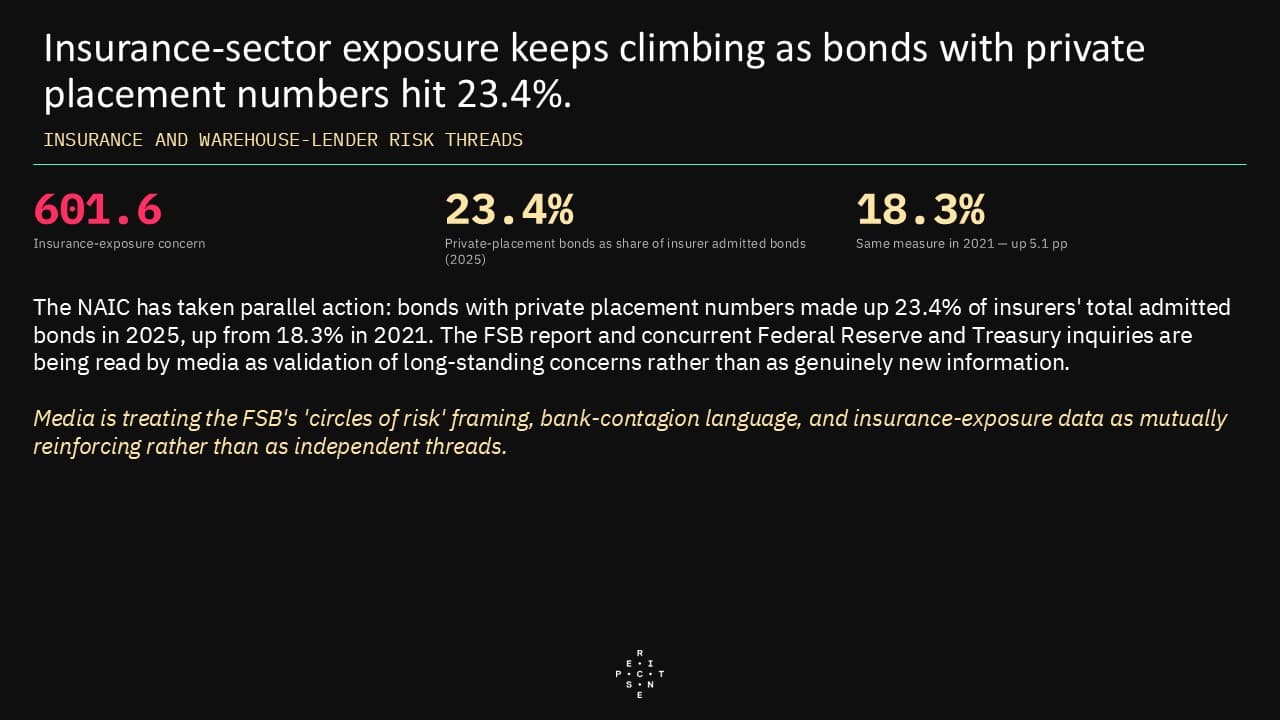

- The FSB's May report and concurrent Federal Reserve and Treasury inquiries catalyzed a synchronized intensification across at least five contagion- and regulation-related narrative threads. Media coverage is treating these developments as validation of long-standing concerns about opaque valuations, "circles of risk" linking banks back to the credit they believed that they had offloaded, and rising insurance-sector exposure—rather than as genuinely new information. The co-movement of stress-testing, bank-contagion, insurance-exposure, warehouse-lender, and securitization-risk language suggests that financial media is consolidating these threads into a single, mutually reinforcing systemic-risk frame.

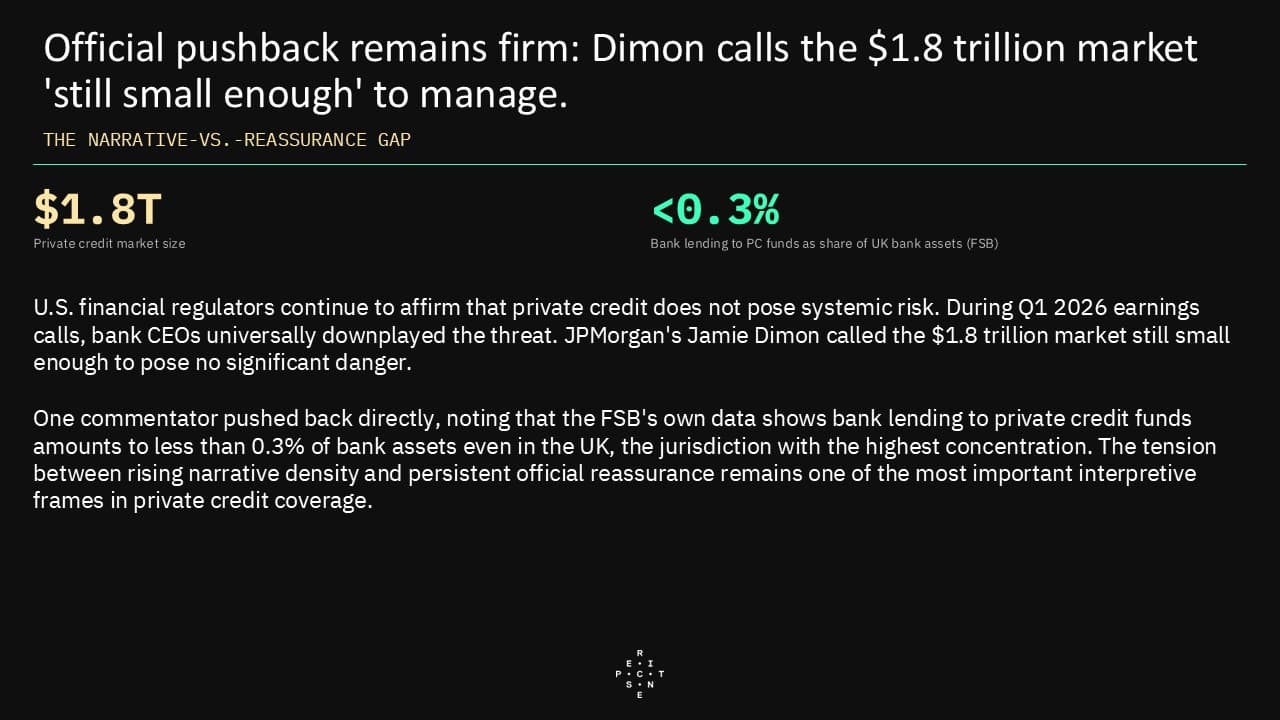

- A widening gap has opened between the density of media language framing private credit as a systemic threat and the persistent pushback from U.S. regulators and bank executives, who continue to characterize the market as too small to pose material stability risk. This tension—rising narrative intensity meeting official reassurance—remains one of the most important interpretive tensions in private credit coverage and complicates any straightforward reading of where consensus is forming.

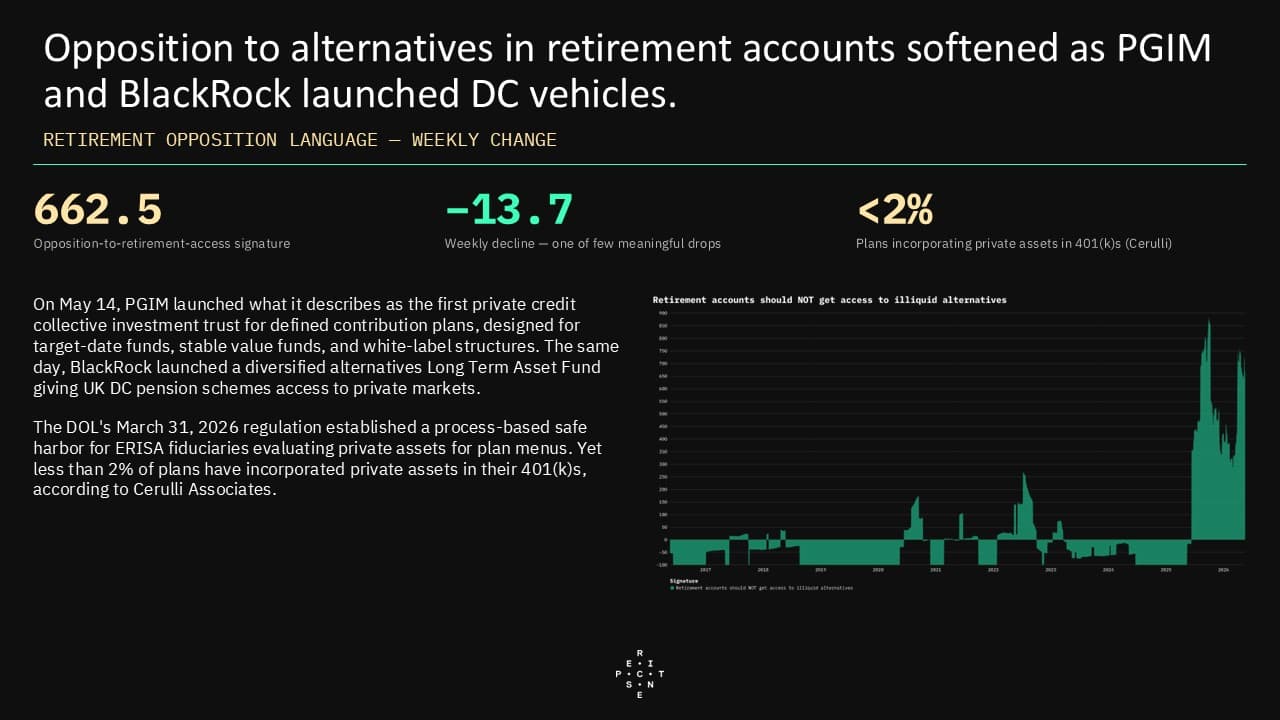

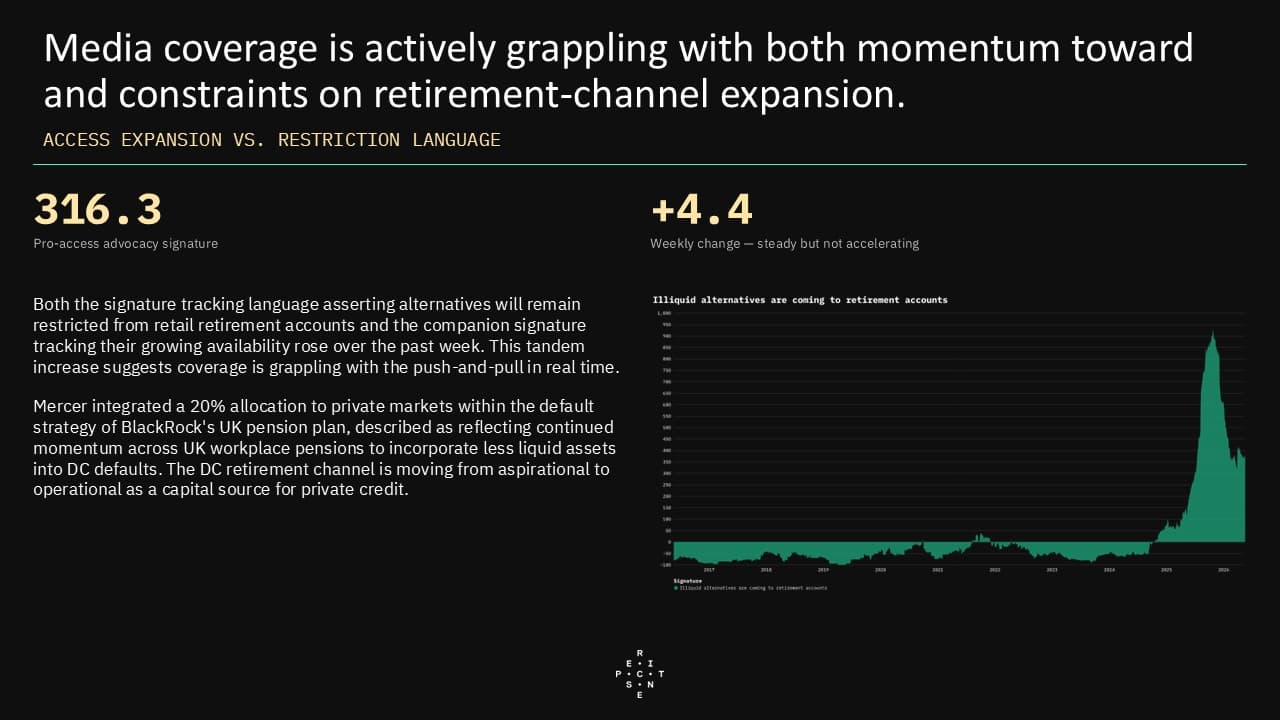

- The retirement-access debate is transitioning from ideological argument to operational reality. Concrete product launches from PGIM and BlackRock are creating actual defined-contribution-channel entry points, and outright opposition language has softened, even though broader concern about retail exposure to private credit continues to climb alongside BDC stress narratives. The fact that opposition language is easing at the very moment that BDC and contagion narratives are intensifying highlights a potential disconnect in media framing.

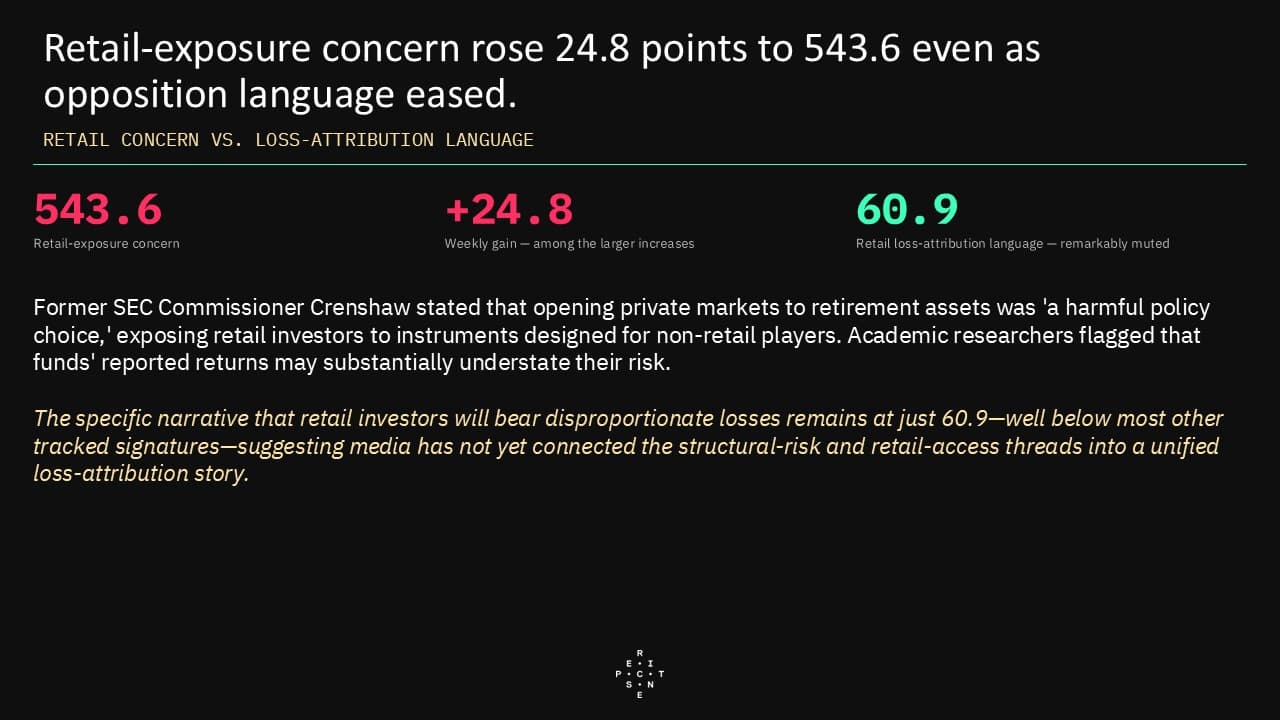

- Despite the escalation of concern language across nearly every category—BDC risk, bank contagion, insurance exposure, regulatory awakening—the specific narrative that retail investors will bear disproportionate losses from private credit remains remarkably muted. This suggests that media has not yet connected the structural-risk and retail-access threads into a unified loss-attribution story, a gap that could close quickly if defaults continue to rise and redemption pressures reach retail-facing vehicles.

DISCLOSURES

This commentary is being provided to you as general information only and should not be taken as investment advice. The opinions expressed in these materials represent the personal views of the author(s). It is not investment research or a research recommendation, as it does not constitute substantive research or analysis. Any action that you take as a result of information contained in this document is ultimately your responsibility. Epsilon Theory will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information. Consult your investment advisor before making any investment decisions. It must be noted, that no one can accurately predict the future of the market with certainty or guarantee future investment performance. Past performance is not a guarantee of future results.

Statements in this communication are forward-looking statements. The forward-looking statements and other views expressed herein are as of the date of this publication. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Epsilon Theory disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein. This information is neither an offer to sell nor a solicitation of any offer to buy any securities. This commentary has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Epsilon Theory recommends that investors independently evaluate particular investments and strategies, and encourages investors to seek the advice of a financial advisor. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives.